Fintechs: the meteor missed but left a tale…

Financial revolutions used to be measured in decades. Even centuries. Now it’s a couple of years, at most.

Financial revolutions used to be measured in decades. Even centuries. Now it’s a couple of years, at most.

Take financial technology companies, “fintechs”. Just a few years back they were the wily, nimble, innovative little mammals about to take over the planet from the doomed dinosaurs of traditional banking.

Jamie Dimon, the chief executive of JP Morgan, the world’s most profitable bank, noted back in 2014 “When I go to Silicon Valley…they all want to eat our lunch. Every single one of (the fintechs) is going to try.”

That sense of threat lasted about two years before it dawned on people that while fintechs had great ideas and technology they lacked scale and capital and, perhaps most importantly, the trust of the broader community.

(Despite Australia, in particular, having a penchant for bank bashing, people trust banks to protect their money and privacy – even if they don’t like them.)

So fintechs started to partner with incumbents – an existential shift given added emphasis when it became clear there was another branch of the technology family that not only boasted innovation and agility but also had scale, capital and trust: “big tech”. Amazon, Apple, Tencent, Google, Microsoft et al.

Critically, those dinosaur banks are now coexisting more happily with fintechs because big techs are a threat to them too. It’s all too easy to imagine a traditional bank customer thinking “Google basically does everything for me, why can’t it do my banking?”

Such is the threat – and opportunity – that nine out of 10 major global financial institutions (including ANZ) are actively pursuing new fintech partnerships to improve their offerings, according to new Finastra research.

This is a well-trod evolutionary path as one-time competitors come to recognise and exploit the competitive advantages both have. Fintechs can partner with banks to achieve scale, banks can harness the innovation of fintechs where they can’t match it themselves.

The Finastra research, conducted by East & Partners, finds the core motivations of global banks to integrate fintech solutions are reducing operational costs (46 per cent), deploying new technology with greater ease (43 per cent) and aligning more closely with evolving compliance needs (37 per cent).

When it comes to lending, survey respondents overwhelmingly viewed fintech partnerships as a vehicle to improve their offering – just a few years ago fintechs were seen as competitors.

“The survey demonstrated the recognition from financial institutions that they cannot navigate these waters alone. They are instead opting to partner with fintechs, with a preference for plugging into a platform of integrated fintech solutions, to help them to adapt quickly while reducing costs.”

-Isabel Fernandez, Executive Vice President of Lending, Finastra

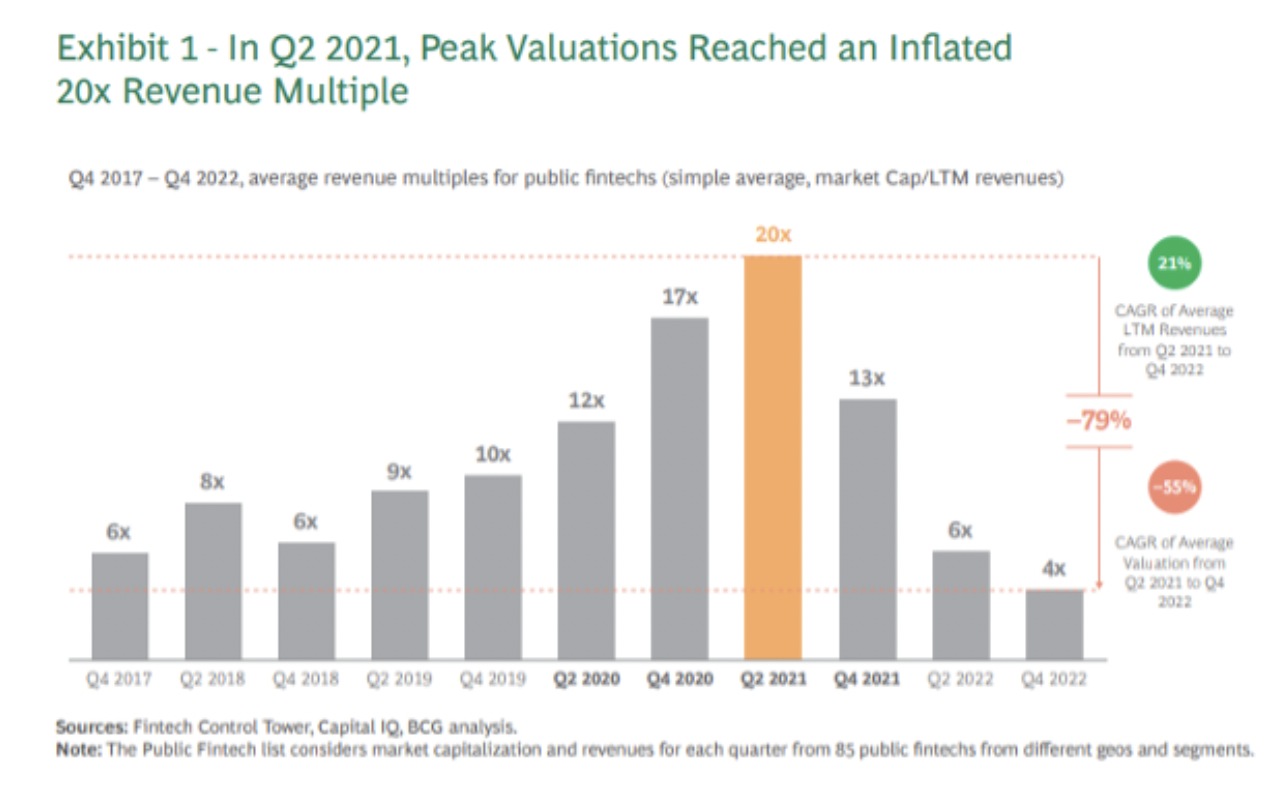

The other driver for fintechs is the vastly different funding landscape compared with pre-2022. Once global interest rates started to rise, valuations of startups and even later stage fintechs began to fall as funding became more expensive and the risk-return trade-off for investors changed.

According to BCG, fintechs on average lost more than half their market value in 2022 – a plunge BCG believes “is a short-term correction in an otherwise long-term positive trajectory, as the industry’s fundamental growth drivers haven’t changed. The overall financial services industry is enormous and very profitable yet struggles with innovation and customer experience.”

The largest fintech market is projected to be Asia-Pacific with 42 percent of incremental revenues, especially emerging Asia (China, India, and Southeast Asia) where fintechs will help expand financial inclusion.

“Incumbents should partner with fintechs to accelerate their own digital journeys and keep pace with consumer expectations.” -BCG

Meanwhile, the competitive threat from the other end of the scale continues to grow. Even if the bigtechs – unlike Microsoft in the 1990s – don’t make a huge fuss about their ambitions, others do.

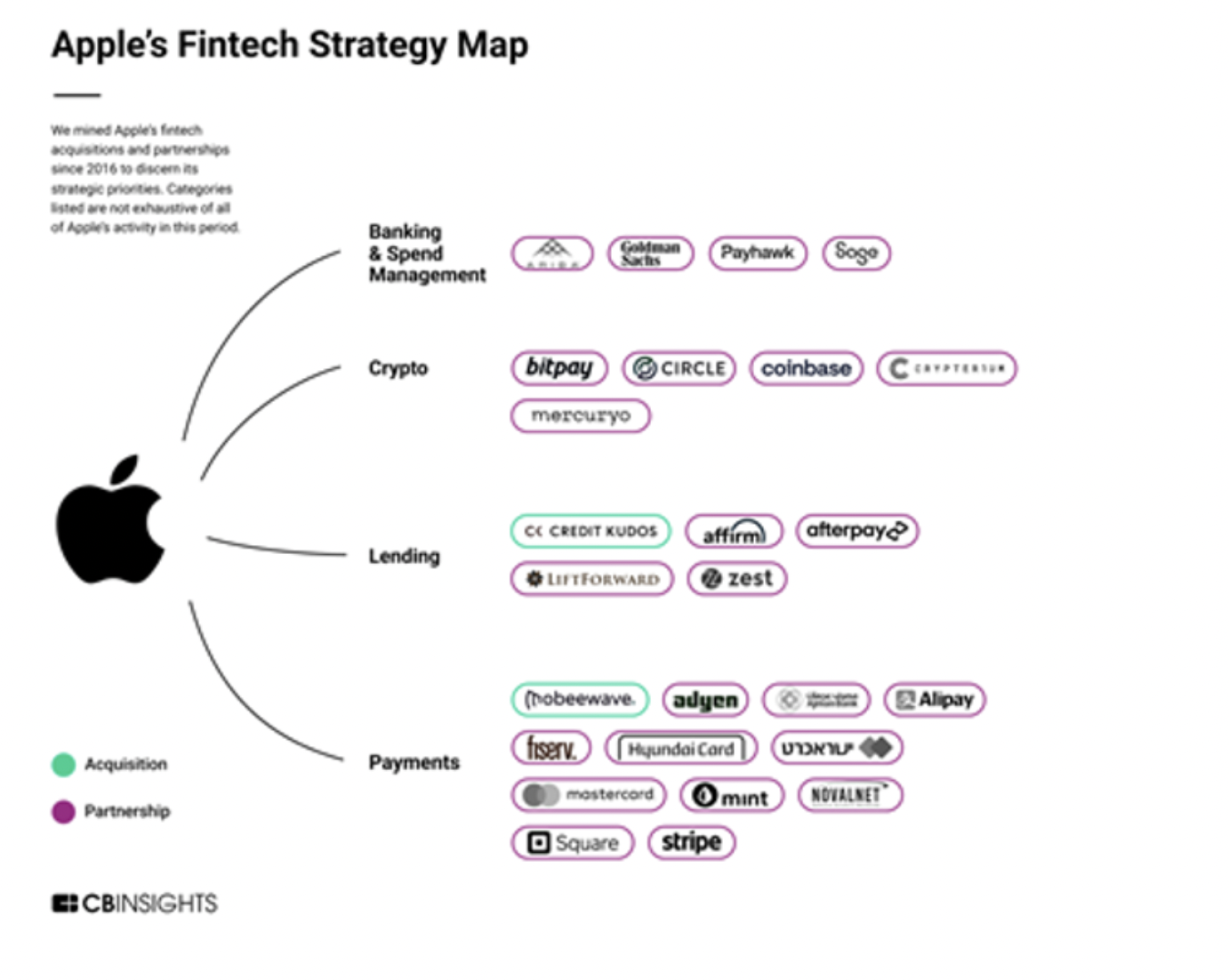

Take Apple. According to technology and venture capital intelligence group CB Insights, Apple has consistently shocked traditional players.

The tech giant sent waves across the fintech landscape last month with the launch of its new savings account, which saw nearly $US1 billion of deposits flow in over the first four days, the firm said.

“While Apple wants to take a bite out of deposits (one of the largest sources of capital for incumbents), there’s so much more to its fintech strategy than a high-yield savings account. From credit cards and instalment loans to mobile and contactless payments, Apple’s fintech ecosystem today poses a growing threat to fintechs as well as banking incumbents.”

Bigtech, in the wake of massive privacy breaches such as Facebook and Cambridge Analytica, does face privacy and trust issues like fintechs but regulators are looking at whether that is warranted or whether some regulatory tweaking could enable innovation in a more trustworthy environment.

The global banking regulator, the Bank for International Settlements (BIS), has just published some research on the theme.

“When designing privacy protection regulation, regulators face a challenging trade-off,” the BIS noted. “On one hand, individuals are reluctant to share their personal data due to concerns about potential abuse or misuse. To protect consumers’ privacy, regulators may consider limiting or even prohibiting the collection of personal data. On the other hand, data plays a vital role for data-intensive firms like fintechs, which rely heavily on personal information to screen and price borrowers. Privacy regulation could thus potentially hinder the growth of fintechs and weaken competition in the financial sector.”

In studying the California Consumer Privacy Act (CCPA) the BIS found a better balance is possible. With greater access to data from a more trusting public “fintechs are able to offer significantly lower loan rates than banks can following the CCPA’s implementation. In sum, the CCPA has benefited consumers by providing fintech lenders, equipped with advanced screening technology, with improved access to data.”

Jamie Dimon noted as much in 2015: “(fintechs) can lend to individuals and small businesses very quickly and – these entities believe – effectively by using

Big Data to enhance credit underwriting. They are very good at reducing the ‘pain points’ in that they can make loans in minutes, which might take banks weeks. We are going to work hard to make our services as seamless and competitive as theirs. And we also are completely comfortable with partnering where it makes sense.”

That’s a view the management of most leading banks today share. Fintechs may not have taken over but they are increasingly living among banks and bigtech. Banks want partners. And even Apple works in partnership with existing banks. Consider Apple Pay or its deposit account backed by Goldman Sachs.

Author: Andrew Cornell, Former Managing Editor at Bluenotes

The views and opinions expressed in this communication are those of the author and may not necessarily state or reflect those of ANZ.

***

This article has been republished with permission from ANZ Bluenotes.

***

If you enjoyed reading this article and would like to be notified when future articles are posted, please sign up for our email newsletter.

Are you interested in reading articles on a particular payments topic, company, payments industry executive or author? Click the search icon, it’s that magnifying glass on the top right-hand side of the website and type in the keywords that interest you. You will then be presented with a list of any articles that match your search criteria.